Introduction

Heading into 2023, the signs of progress that appeared over the past year continue to blossom. The organizations that have made it through recent and ongoing turmoil are using their newfound resilience as a springboard into the future. The return to strategy predicted by CompTIA’s IT Industry Outlook 2022 has become a reality for many organizations, and they are now focused on writing their next chapter.

Those new chapters hold a tremendous amount of potential. Spurred by global events, companies may decide to focus more effort on improving the world around them. There are clearly big problems to solve; what may be less clear is that many solutions already have good momentum. According to the 2022 Goalkeepers report from the Gates Foundation, the percentage of the global population living below the international poverty line has fallen by nearly 20% since 2015, and the rate of mortality for children under 5 has fallen by more than 50% since 1990. Organizations that choose to make an impact on social issues can help drive greater improvement.

Closer to home, there is potential for individual company growth. The modern business world is far less constrained by geographic reach, financial backing, or language barriers. Organizations have more opportunities than ever to diversify their workforce, reach new customers, and develop new products. Whether expanding current offerings or pivoting to a new business model, companies can build on lessons learned to reach new heights.

No matter which direction an organization may choose, technology will play a starring role in the story. Technology alone cannot solve all the world’s problems, but it can accelerate solutions for those with the right vision. The technology industry may face future headwinds around ethical concerns or regulatory maneuvering, but there is no doubt that those hoping to make a difference can use technology to unlock the potential they imagine.

Trends to watch in 2023

- Business as usual gets a hard reality check

- Worker-employer relationship gaps expose new challenges in hiring and retaining tech talent

- Metaverse initiatives will focus on holistic customer experiences

- Cloud acceleration drives demand for orchestration and FinOps

- New players in the digital ecosystem put more competitive pressure on established practices

- Vendors and partners eye greater automation with optimism – and concern

- Cybersecurity metrics are tied to an evolving risk analysis approach

- Inflation uncertainty and supply chain issues continue to complicate sales forecasting

- Decentralized identity will become the heart of Web3 efforts

- Advances in AI spur debate over the value of content

Industry overview

The importance of technology in our modern world means that the technology industry is a true force to be reckoned with. The sheer size of the industry makes it one of the dominant sectors in the global economy, and the rapid growth and rate of change within the industry make it a central player in developing business standards and regulations.

The impact of technology goes far beyond the core tech industry, though. While there are myriad opportunities directly related to digital product development or service delivery, countless more opportunities are opening up around the world as technology influences every business and every industry vertical.

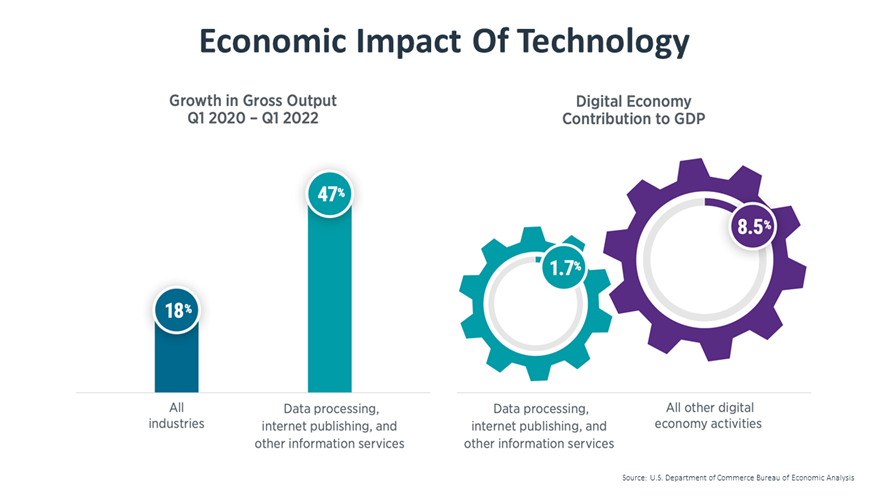

To start, consider economic output. According to the Bureau of Economic Analysis (BEA) within the U.S. Department of Commerce, overall GDP grew by 18% between Q1 of 2020 and Q1 of 2022. In contrast, the sub-industry that most closely represents the core tech industry (Data processing, internet publishing, and other information services) grew by 47%. This growth rate trailed only two sub-industries related to oil and petroleum; many other sub-industries grew at much slower rates or experienced contraction during this time.

Although that growth alone is noteworthy, it pales in comparison to the extended impact of digital activity. As of Q1 2022, the same sub-industry contributed to 1.7% of overall U.S. GDP. Looking across industries in three broad categories of digital economic activity (infrastructure, e-commerce, and priced digital services), the BEA estimates that the overall digital economy contributed 10.2% of the U.S. GDP in 2020. Roughly speaking, the extended digital activities taking place outside the core IT industry have five times more impact than direct tech industry activity. The exact numbers differ from country to country, especially in maturing economies vs. mature economies, but the basic premise holds that technology has a massive direct and indirect impact on economic growth.

A second area to consider is the workforce. According to CompTIA’s State of the Tech Workforce report, technology was expected to account for 8.9 million jobs in the United States in 2022. This represents both those individuals working directly within the tech industry and those individuals in core tech occupations within other industries. With a labor force of just over 158 million workers, direct tech occupations account for nearly 6% of the U.S. workforce.

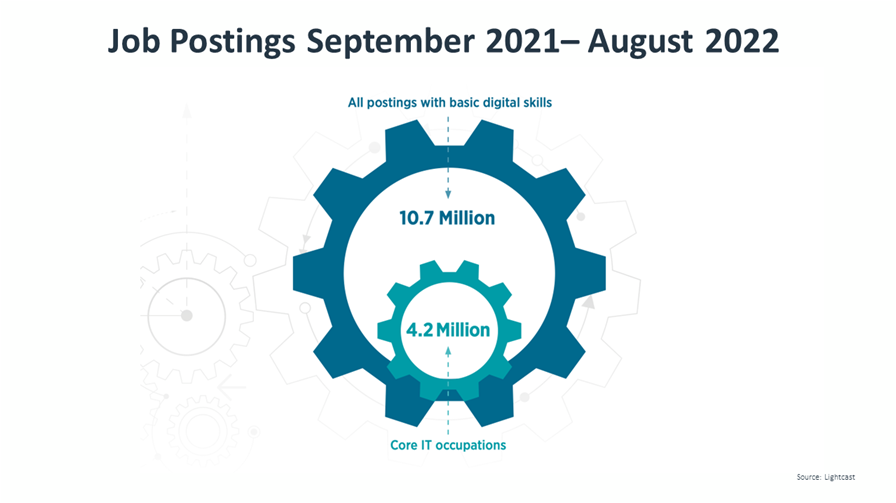

Once again, the impact of technology extends far beyond these numbers. Examining job postings from the labor analysis firm Lightcast, there were 4.2 million job postings for core technology occupations between September 2021 and August 2022. Over that same time period, there were 10.7 million job postings requesting skills in basic computer literacy and productivity tools such as Microsoft Office. Of the top ten occupations within the 10.7 million job postings, only computer user support specialist is a core tech occupation. Other occupational categories include managers, human resources specialists, and registered nurses.

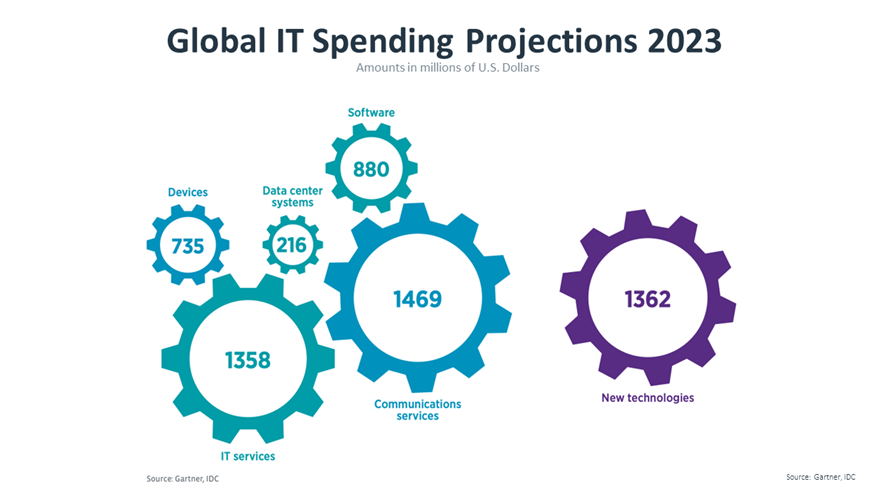

Finally, the amount organizations are spending on IT demonstrates the rapidly changing nature of technology. Gartner estimates that 2023 global IT spending will reach $4.6 trillion in 2023, a jump of 5.1% over 2022 spending. The categories included in Gartner’s estimate are traditional IT components: Communications services, IT services, devices, software, and data center systems. As expected, the service categories are the largest pieces, as most organizations have built a foundational layer of computing and are now crafting new solutions on top of that foundation.

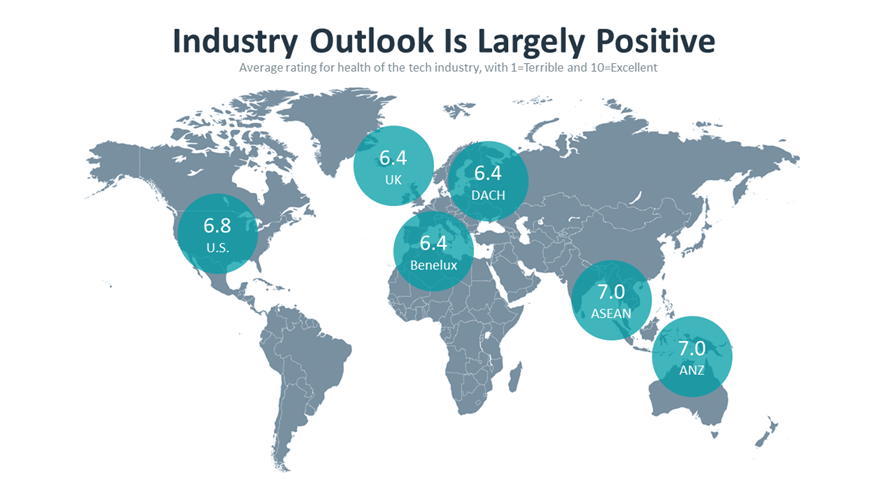

Given both the direct and indirect impacts of technology, it is no surprise to see positive sentiment toward the industry. Among technology firms in each of the six different geographic regions surveyed by CompTIA, the average rating for the future prospects of the overall technology industry skewed toward the higher end of the scale. Even with economic uncertainties and societal issues, the tech industry remains a robust choice for business growth and career advancement. For the remainder of this report, the focus is on U.S. data. Separate research briefs highlight data points from international regions.

All in all, the impact of technology today goes far beyond the technology itself. Technology is deeply ingrained into business activity and daily life. There is no question that there are some negative elements, especially as technology applications reach massive scale and trigger unintended consequences. However, there is also no question that there are many positive outcomes, and a progressive approach to technology is a critical factor for sustained success.

Careers in technology: Building strategic skills

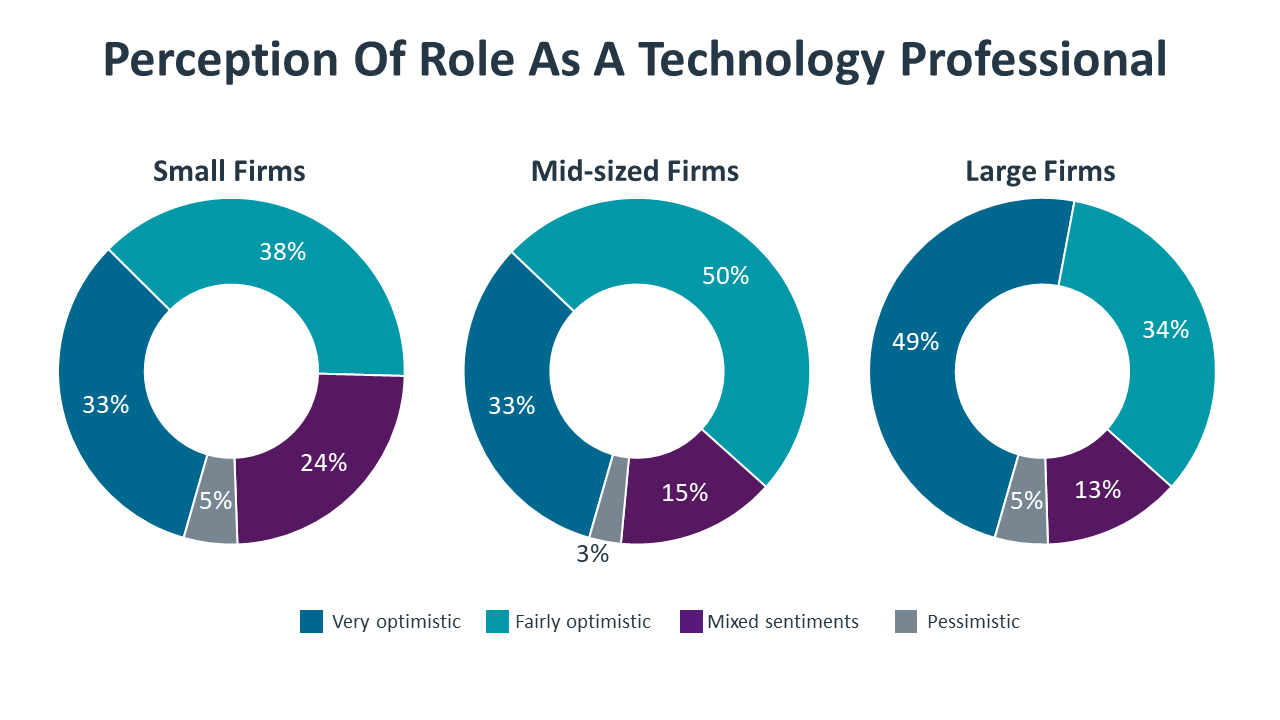

Caught between the recent disruption of the pandemic and the potential upheaval of a recession, technical professionals share many concerns with the rest of the workforce. However, the turmoil is not dampening spirits for IT pros. As with last year, nearly 80% of IT professionals in CompTIA’s survey report feeling optimistic about their role, including 38% who feel very optimistic. Positive sentiments are correlated with company size; 71% of IT pros feel optimistic at small companies (less than 100 employees), compared to 83% at both mid-sized firms (100–499 employees) and large enterprises (more than 500 employees). In addition, nearly half of all respondents at large enterprises report feeling very optimistic about their role.

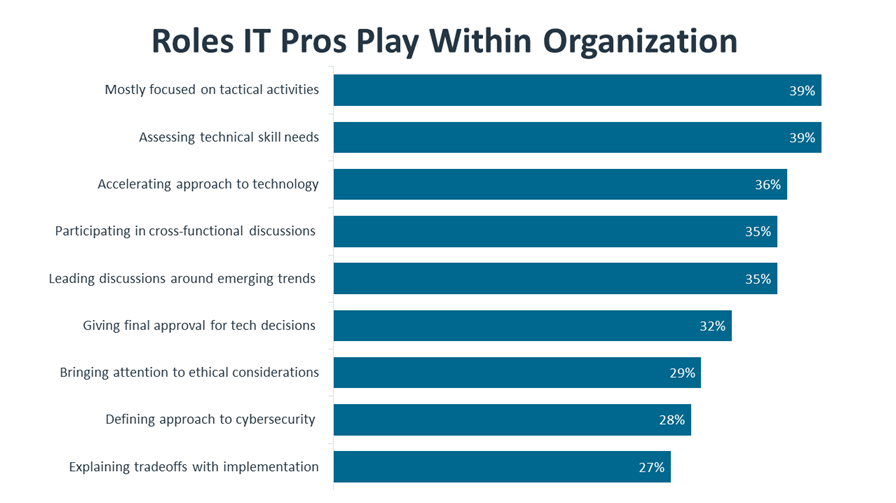

A likely explanation for higher optimism at bigger companies is the wider range of opportunities. Given the historical view of IT as a supporting function and the daily pressures that most companies face, it is no surprise to see that the top focus for most IT pros is tactical. Servers still need to be available, and help desk tickets still need to be answered. Beyond this traditional role, though, there are more strategic areas for IT pros to explore, including skill assessment across the organization, improving the cultural mindset around technology, and leading discussions across departments regarding technology adoption or future trends.

The profusion of opportunity is not just something organizations are doing to help their IT employees. With technology now acting as a critical component in business strategy, it is in a company’s best interest to integrate its IT specialists more deeply into operations. Of course, with most organizations making this move, the demand for skills is outpacing available supply, meaning that opportunities are open not only within an IT pro’s current employer but also in other firms that may provide higher pay or better flexibility. Over the past year, technology job postings have been plentiful, and tech unemployment has been incredibly low. There is no reason to expect a huge change in the situation in 2023.

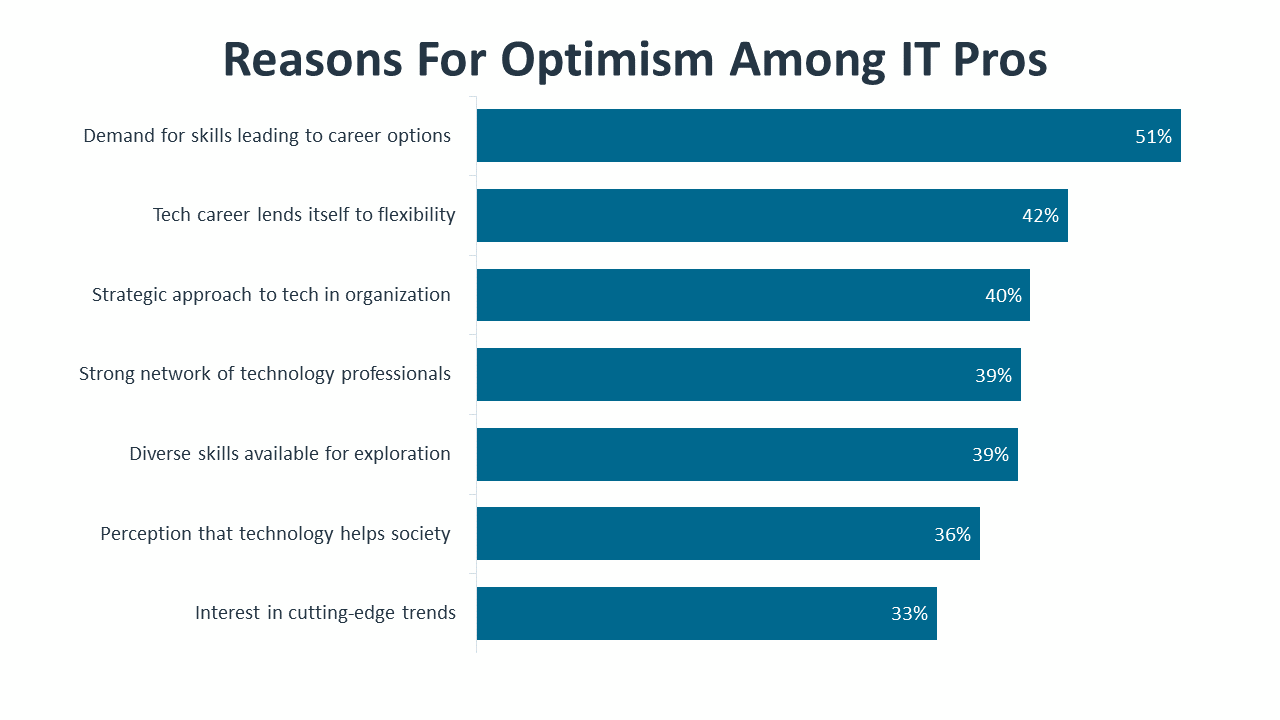

This high-demand environment is commonplace today, but it is a relatively new phenomenon for IT professionals. In the early days of enterprise technology, most organizations did not need technical skills. Computing was reserved for the largest companies with the biggest budgets. As technology became more widespread, the IT function was largely viewed as a cost center, and IT pros were often constrained in both resources and career progression. In today’s environment, companies view IT through a strategic lens, increasing both their appetite for technology and their investment. This then leads to a high demand for skills, creating a broad range of career options, which is the top reason for optimism.

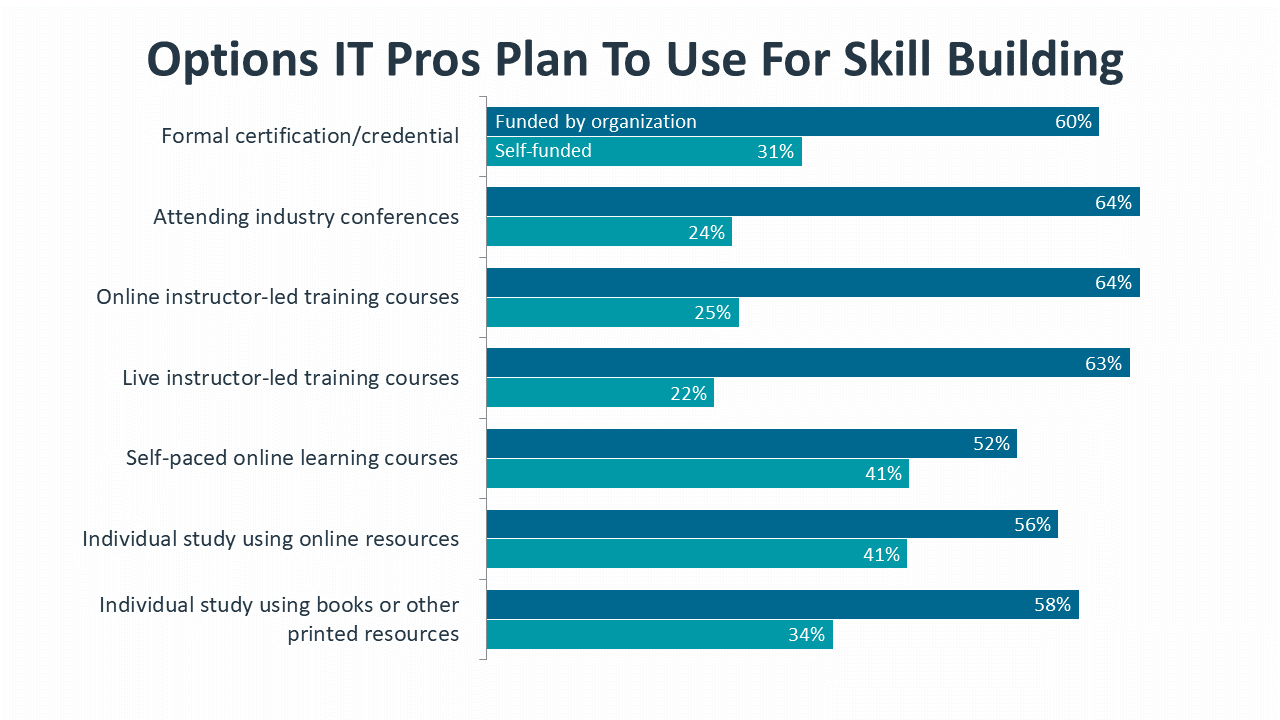

As described in the trends section, the abundance of choice opens a new set of questions. This is true for IT pros as much as it is true for companies procuring technology products and services. With many options for career advancement, there are also many options for building skills. The top choice for many technologists is to develop skills within their current area of specialization. Beyond that, durable skills such as communication or teamwork are beneficial as technology becomes more of a team sport. Rounding out the top three focus areas, IT pros may choose to explore a new area as businesses explore topics like data science or zero-trust architecture. Many new job openings require a mix of various skills, and technical specialists in one field may only need to add a few new skills to become fluent in another discipline.

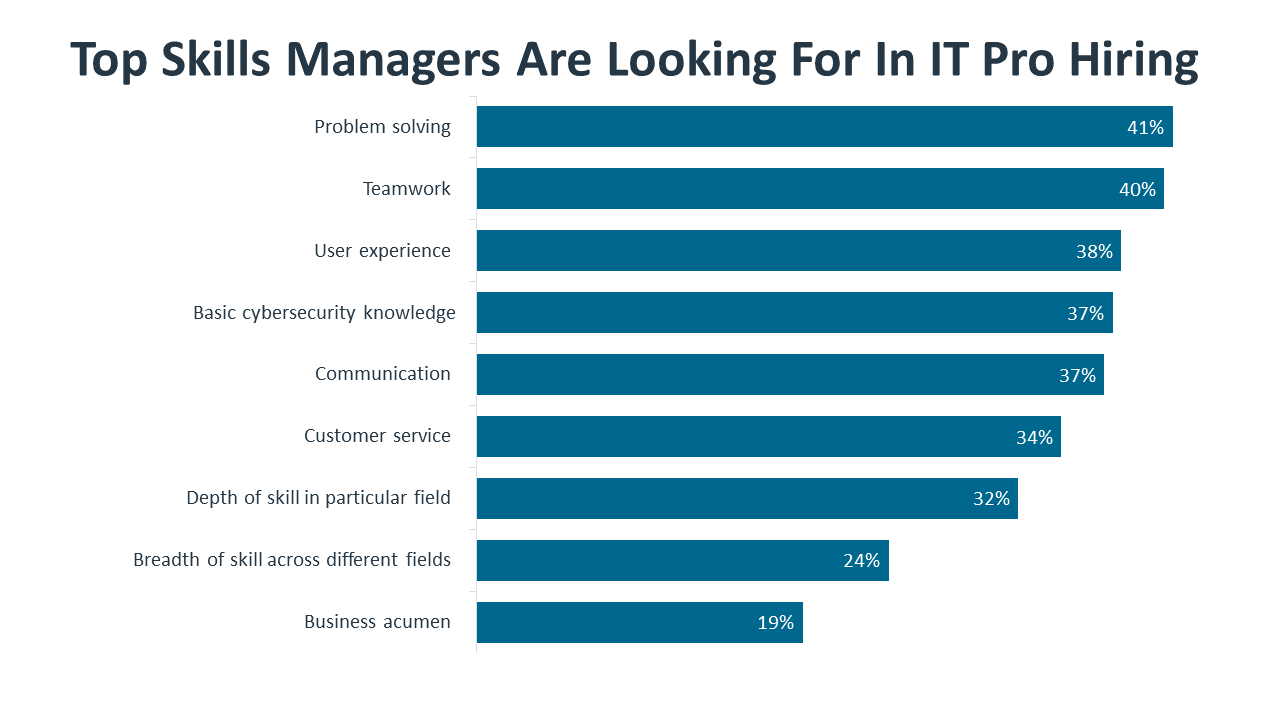

Whether the choice is developing skills within a current specialization or exploring a new opportunity, there is no shortage of skills needed in digital organizations. The many different facets of enterprise technology can be captured in four broad categories. CompTIA’s IT framework defines infrastructure, software development, cybersecurity, and data management/analysis as the pillars that support IT operations. At this high level, the top priorities for the coming year are software development and data management/analysis. This fits with a viewpoint of companies tailoring technology as it becomes more strategic, but that does not minimize the importance of infrastructure and cybersecurity as foundational pieces of digital transformation.

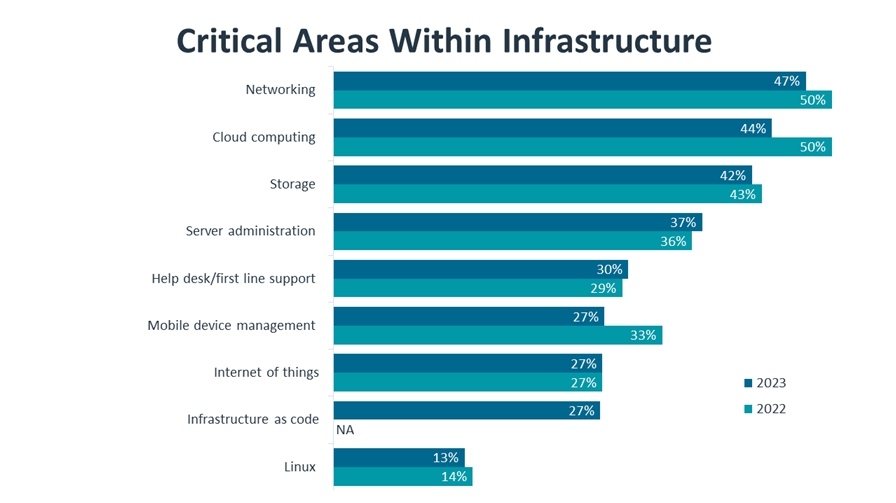

In the area of infrastructure, priorities remain fairly consistent with last year’s agenda. The ongoing maturity of cloud operations will drive demands in the areas of networking, storage, and server administration. As cloud orchestration becomes more important, there will be a stronger desire for more advanced skills in each of these fields. Mobile device management takes a step backward this year as there is likely less focus on equipping the workforce and infrastructure as code (IaC) makes an initial appearance as organizations place more emphasis on software-defined data center operations.

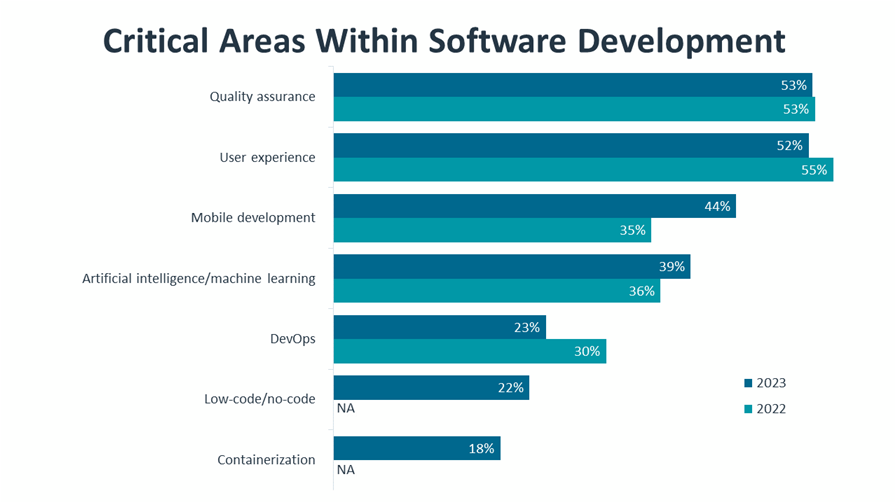

The domain of software development is also not experiencing drastic year-over-year change. As organizations expand the number of customized applications for both internal and external use, there is still a high focus on quality assurance (QA) and user experience (UX). With mobile devices steadily accounting for half of all internet traffic, optimizing digital experiences for mobile consumption continues to be important. IT pros are predicting less focus on DevOps in 2023, but this is largely because DevOps practices have now become firmly established within many firms, driving a constant demand for skill but not new investment or restructuring. Low-code/no-code solutions and containerization expand the reach of software and create more abstraction in the development process, and those areas are both expected to grow in importance in the coming years.

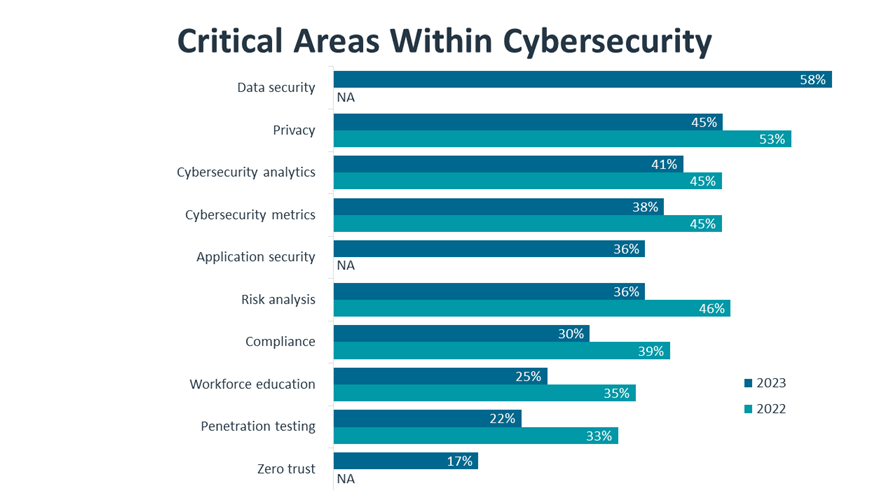

The fields of cybersecurity and data management/analysis are newer specializations for many companies, so there is more churn when it comes to focus areas. In cybersecurity, the acknowledgment of a shift away from a secure perimeter into a more granular approach is finally becoming widespread and causing policy change and upskilling needs. Data security and application security were new options in this year’s survey and clearly demonstrate how companies are reimagining their cybersecurity posture. Aside from these two new areas, focus seems to be dropping across the board for cybersecurity topics. This disconnect was explored in depth in CompTIA’s 2022 State of Cybersecurity report, and it signals that companies should put more emphasis on integrating cybersecurity with organizational objectives. One specific area to keep an eye on is risk analysis. As businesses try to determine the proper level of investment for cybersecurity initiatives, risk analysis will likely be the framework guiding decisions. Along the same lines, zero trust is not currently a defined approach for many organizations, but elements of a zero trust architecture are seeing more and more adoption.

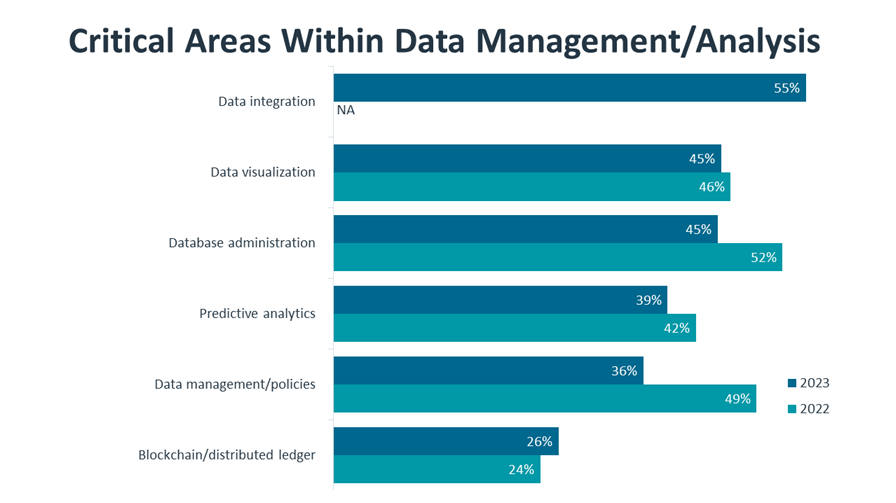

Integration is also a new concern in the area of data management/analysis. While many companies still need to focus on fundamental database administration in order to create a foundation for advanced data activities, data integration is becoming the overarching process that defines how data will be combined from various sources and made available for consumption and analysis. Analytics (and eventually data science) is still the end goal, but bringing the data into a comprehensive starting point is still a major challenge. Distributed ledger technology, such as blockchain, is slowly making inroads as an enabling technology, and it may be some time yet before the technology moves from isolated applications to broad usage within data structures.

While intent to hire is still strong (44% of companies expect to hire for technical skills in 2023), internal training remains the dominant option for closing skill gaps (64% of companies expect to train existing employees in 2023). In considering workforce development options for the next 12 months, companies may need to invest more heavily in certain components. A rigorous skill assessment can pinpoint the specific skills needed to advance corporate objectives, and it can also define training options that can target those skills. Getting closer to the actual training program, businesses can expand the types of offerings that are provided or subsidized in order to ensure the best pathways for individual learning styles.

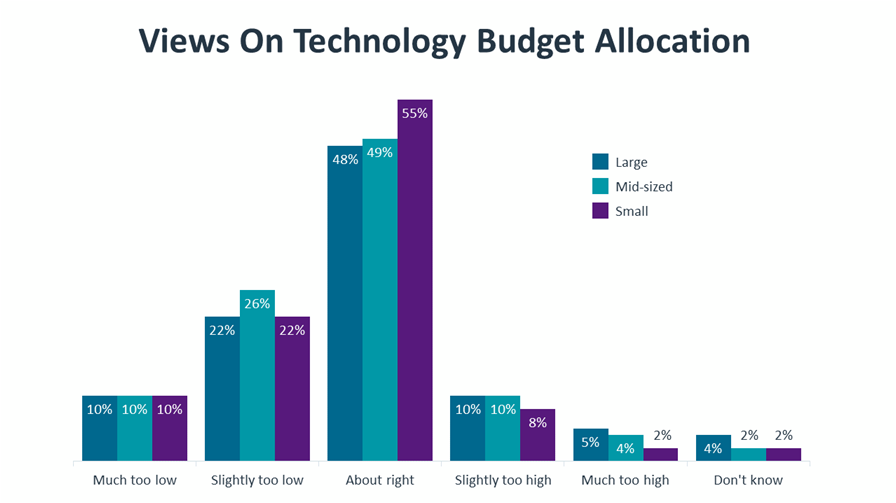

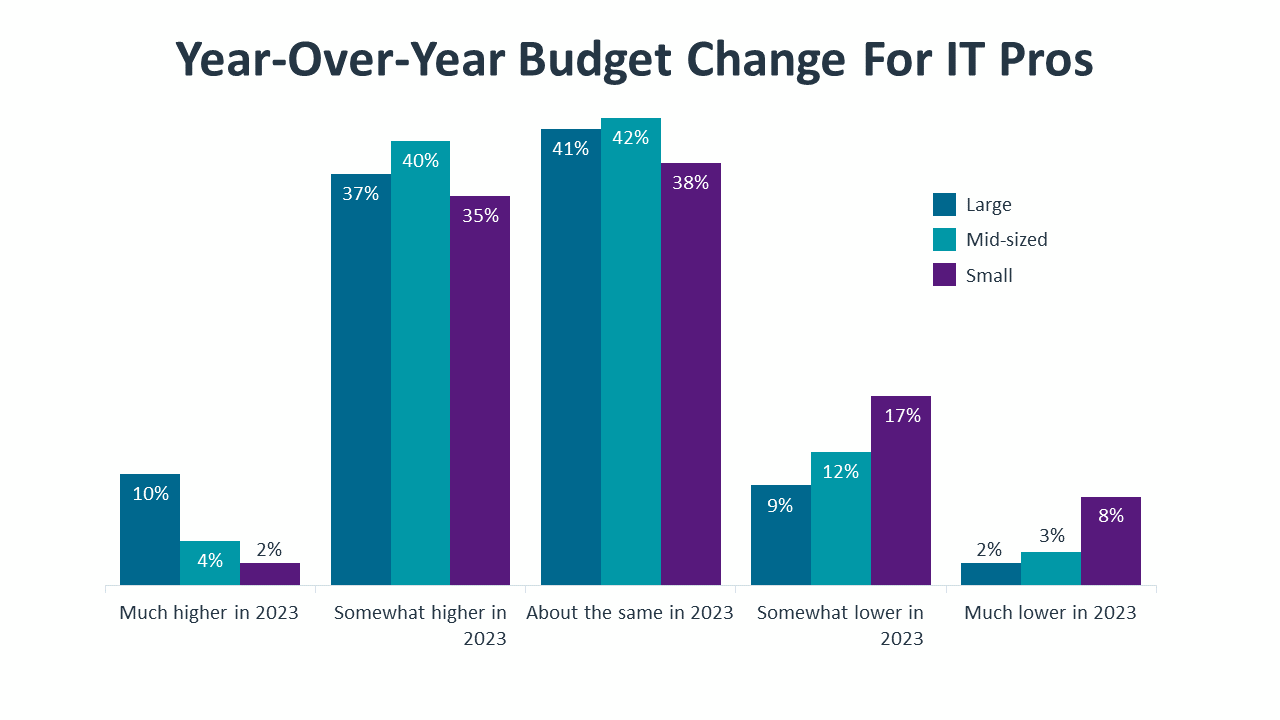

These investments for workforce development are obviously part of the larger technology budget, which appears to be stabilizing at adequate levels for most companies. As expected, the perception of technology budgets skews toward the insufficient end of the scale. Overall, though, the technology budget is healthy for most organizations, and it is moving in the right direction; 43% of companies believe that their technology budget in 2023 will be higher than it was in 2022.

At first glance, it may seem strange that any IT professionals would believe that the technology budget is too high. While there are only a small number of individuals in this category, it is worth exploring the sentiment. Given that this viewpoint is slightly more prevalent in larger firms, this may be a statement on balance. In an environment where digital transformation is held up as a new business imperative, organizations may begin viewing technology as a cure-all, opening the wallet for advanced technology purchases without making corresponding investments in best practices for usage or restructuring of business flow.

This may be exacerbated by business units making their own technology investments. When asked to consider how the overall technology budget was divided between the IT function and business units, IT professionals in CompTIA’s survey reported a nearly even split, with a slight lean toward business units. Technology procurement by business units is not necessarily a problem (and also not exactly something that can be avoided), but it does require close collaboration. A particular business function may be closest to the situation and best able to define functional requirements, but areas such as cybersecurity and integration likely fall outside the technical expertise of business unit employees.

One of the most useful questions for ranking technical priorities might be how to spend additional money if new funds become available. This leaves the field open-ended rather than focusing on an individual topic, and it still provides some degree of constraint given the financial context. Case in point: Automation ranks relatively low in this scenario, whereas most organizations give high marks to automation when automation is the only topic of discussion.

The tier above automation and collaboration tools contains a mixture of wish list items. There are fairly traditional topics like web presence and cybersecurity alongside a newer topic in data analytics. The desire for a new headcount shows up here, even as skill gaps are similar to automation as a top-of-mind issue in a vacuum. With these items so tightly clustered, the exact priority will depend on the specific needs of an organization.

Moving to the top tier, it is somewhat surprising to see endpoints ranked so highly. Given the large investments made to enable a remote workforce over the past two years, one might assume endpoints are up to date. This high priority speaks to the critical need to keep the workforce productive. Minor glitches with laptops or smartphones can lead to major disruptions in employee productivity.

It is no surprise, though, to see innovation in the top slot. Whether it is investing in new products, bringing in third-party expertise, or creating platforms for technology evaluation, IT professionals believe that accelerating the approach to technology will be the biggest differentiator for their organizations. Day-to-day maintenance and improvements are needed for operational progress, but the cutting edge is where the potential is fully unlocked.

Emerging trends: The next step for digital solutions

Innovation, like so many other things, is easier said than done. After years of a product-centric view of IT, organizations are struggling to build a new mindset around emerging technology. Rather than acting as standalone products that meet specific needs, emerging trends are more often found as enabling parts of broader solutions. The question is not so much “What can this technology do for us?” but rather “What are we doing that could be made better through technology?”

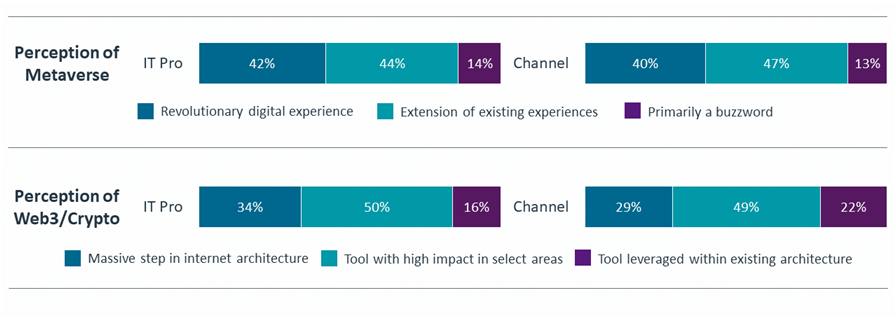

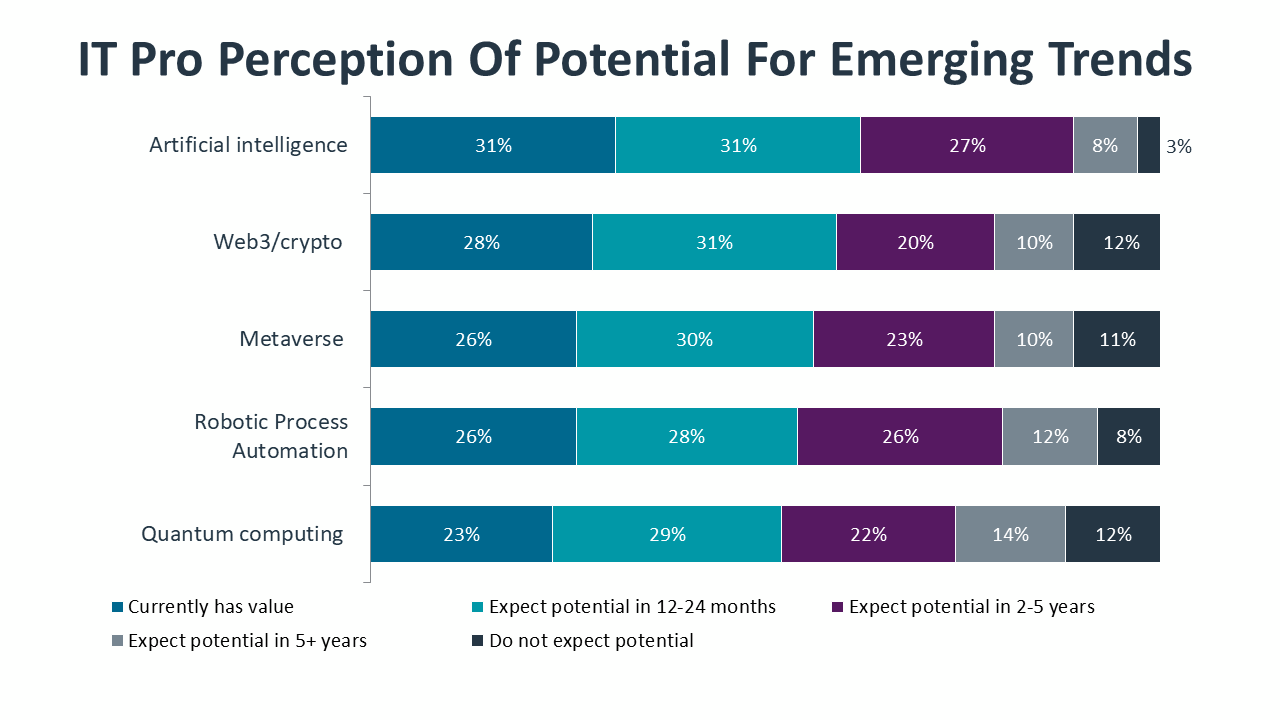

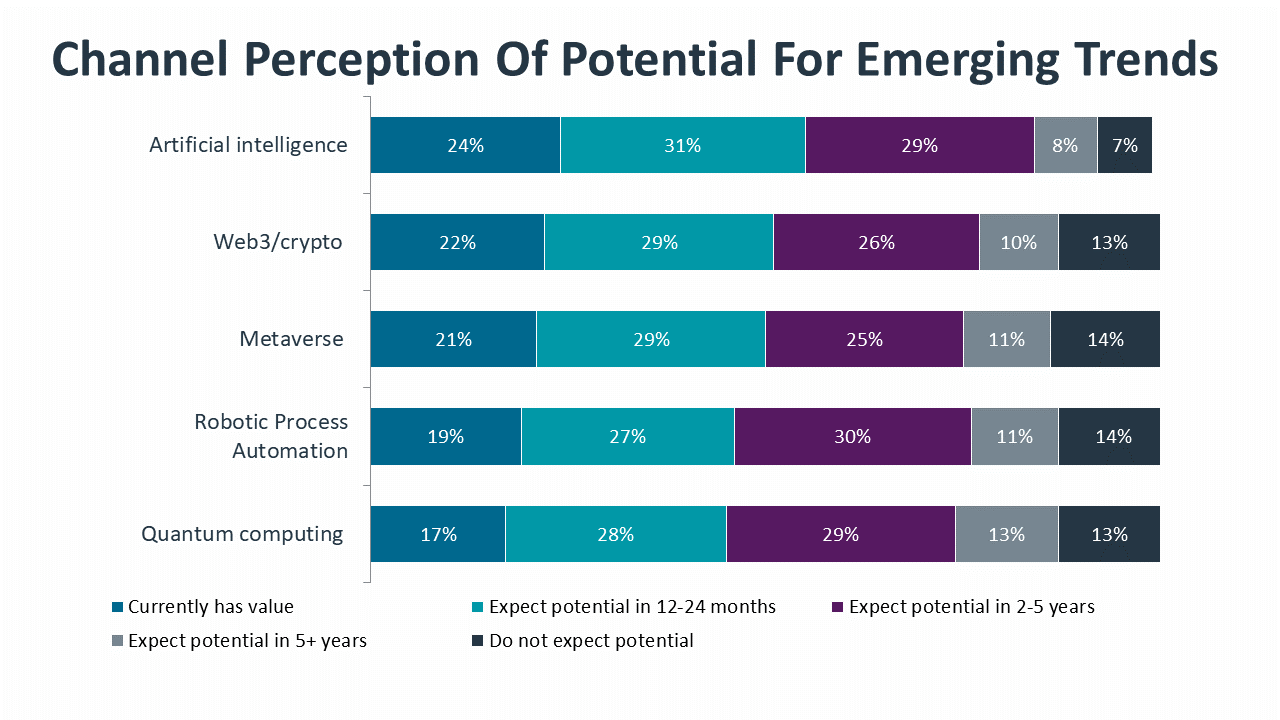

Two of the latest trends on the horizon illustrate this point. For both the metaverse and Web3, the perceptions from both IT pros and channel constituents highlight how the long-term outlook may differ from disruptive predictions. These two groups, which are the closest to technology and have navigated previous waves of emerging trends, are very aligned in their viewpoints. Most significantly, the majority opinion is that neither technology will likely be a revolutionary step forward. Instead, they will both augment digital experiences and solution architecture.

Aside from adopting a more comprehensive mindset, the challenges around emerging trends center on integration and utility. As new technology develops, standards and regulations become a defining factor in implementation, driving demand for technical skills across the entire ecosystem. In addition, building an appreciation for the strategic use case requires an overall understanding of business objectives and skills in education and marketing.

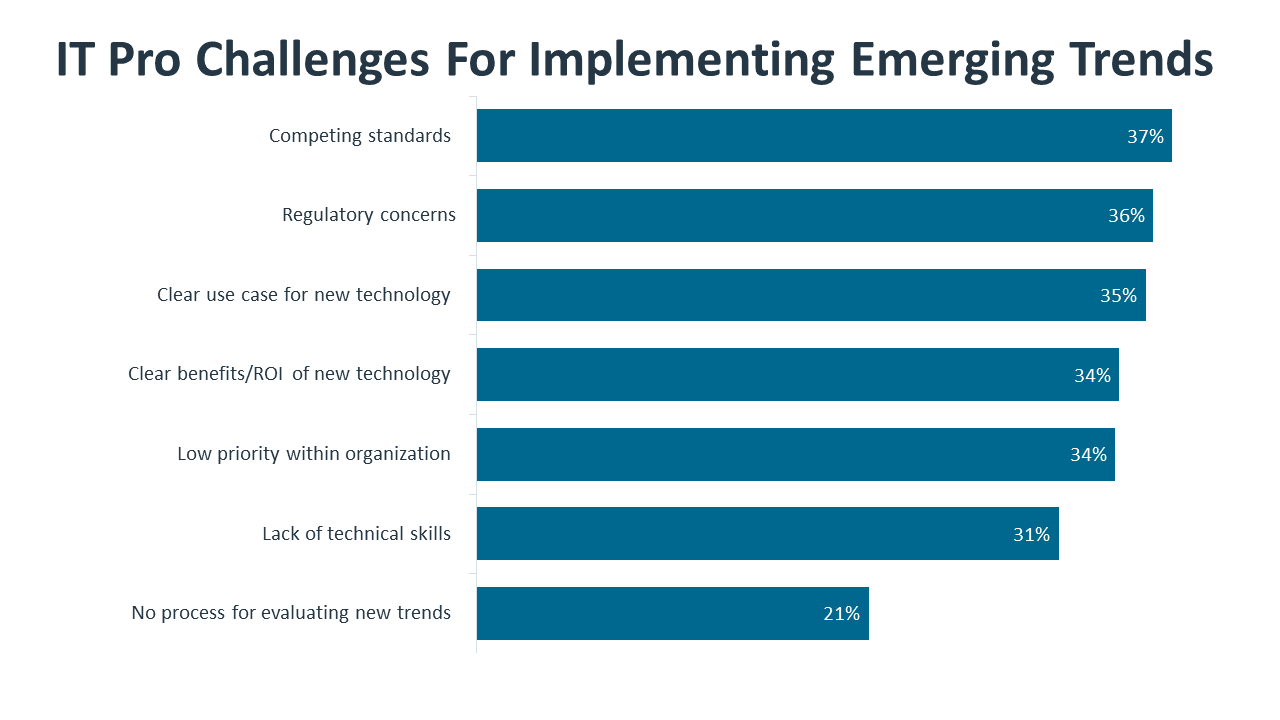

Top IT pro challenges for emerging trends

- Competing standards

- Regulatory concerns

- Clear use case for new technology

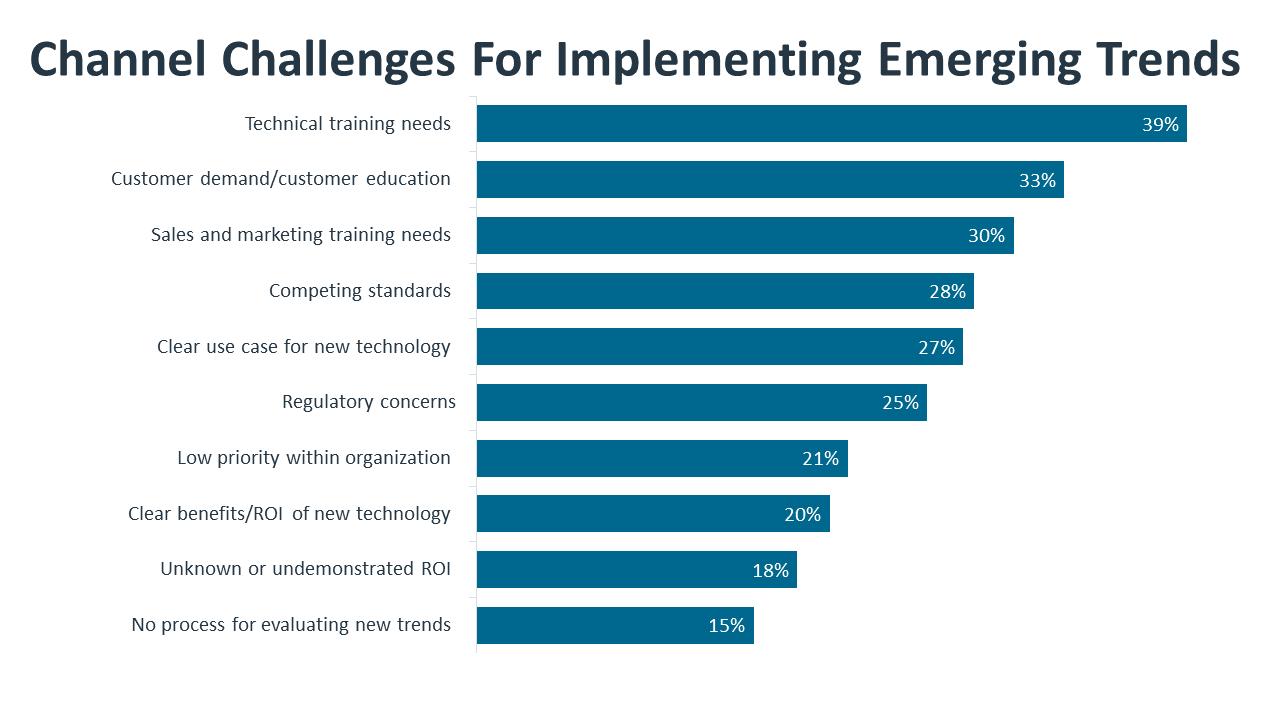

Top channel challenges for emerging trends

- Technical training needs

- Customer education

- Sales and marketing training needs

The business of technology: Forging ahead in tough waters

Much like IT professionals, companies in the business of technology (aka the channel) are starting to think bigger again, rekindling some of the strategic initiatives and aspirations that may have been put on the back burner during the extended pandemic. Yet there is trepidation as well, with many channel firms of all stripes worried about continued inflation, supply chain issues, and the omnipresent threat of an economic recession. It’s a paradoxical time as we look ahead to 2023, one in which companies are at once ready to forge ahead with new investments and innovations yet must do so with a dose of caution attributable to the uncertainty of the business landscape.

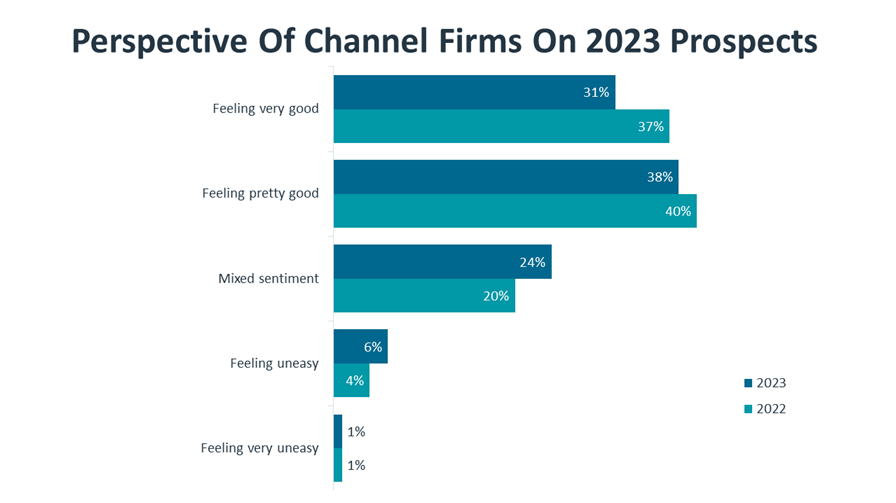

This dilemma is reflected in general attitudes about the year ahead. For the most part, channel firms remain positive about their own company’s outlook for 2023, although the numbers have dipped from last year. Sixty-seven percent of respondents said they are feeling either very good or pretty good about 2023 compared with 77% that said the same last year about 2022. Instead, more channel firms have adopted a mixed attitude about how their company will fare in 2023. Twenty-four percent said they are on the fence about how 2023 will go vs. 19% that said the same last year. This sentiment reflects the guessing game situation many companies find themselves in today as they weigh new investments and hiring against continued inflation and a potential recession.

Breaking things down a bit more, channel respondents save their most pessimistic attitudes for the current state of the overall economy, compared with the IT industry and their own businesses. While 9% rate the overall economy as “terrible” (the lowest score of 1 on a 1-10 rating scale), just 2.6% confer that dispiriting take on the IT industry and only 1% on their own businesses. There’s a disconnect, for sure, but one that makes sense based on three years of a pandemic in which other parts of the economy suffered greatly while the tech sector held its own and, in fact, thrived in many areas. Responses from the most positive end of that 1-10 rating scale bear this reality: While 8.6% of respondents gave the overall economy a “best” or 10 ratings, 12% did so for the IT industry and 15% for their own businesses. It’s important to note that these numbers reflect the two extreme ends of the scale (bad and good), while most respondents fall in the middle in their assessments of all three areas of the economy.

One of the markers that channel firms will be looking for in the year ahead is the growth potential of their own business in relation to the tech industry at large. Many are bullish and believe that growth potential is strong. Forty-five percent of respondents said they expect their own revenue and profitability numbers in 2023 to exceed those of 2022 if the tech sector flourishes. A more cautious 44% of respondents said they expect stable results on par with the previous year, even if the tech sector does well. And finally, roughly 8% said they still expect a decline in revenue and profitability even if the tech industry performs on the positive side of the economic equation. Those predictions are correlated across all company sizes, from the smallest channel firm (fewer than 10 employees) to those with more than 500 staffers.

Hedging one’s bets is normal behavior in an uncertain economy, but the reality is that the tech industry and the businesses that operate in it have opportunities galore in the year ahead. It’s a matter of unlocking that potential wisely. A few truths to consider: The industry itself is more complex and changing rapidly at both the technology and business levels. From the channel’s vantage point, that means their expertise will be in demand and greatly valued. The tech portfolio has changed immensely, too. What was once a stable set of infrastructure products on a reseller’s line card has, in the cloud age, morphed into a cornucopia of software-as-a-service applications, data and cybersecurity tools, and a stack of emerging technologies to contend with. At a business model level, everything’s in flux as companies transition into various forms of service providers, referral or influencer agents, consultants, or a combination of all. Finally, one of the most consequential developments affecting the channel today is the changing customer, specifically their procurement habits and technology preferences.

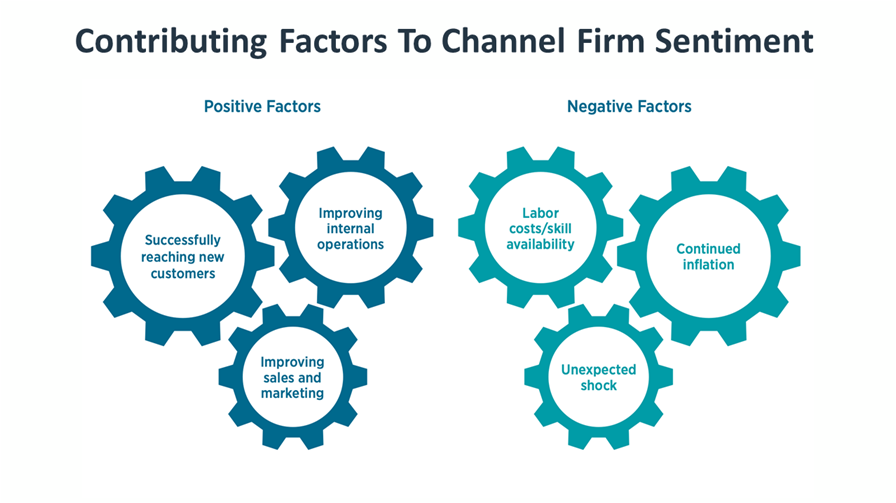

So, what are some of the keys to unlocking that growth and potential? Respondents cite many factors that will help lead to an optimistic performance in 2023. Leading that list is the ability to drum up business from new customers. Nearly 4 in 10 respondents said this will be critical to solid performance in the year ahead. This signals a change in emphasis from the early pandemic years when companies’ focus was on retaining and expanding business with existing customers. That pursuit is still a prominent aim (28% cited it), but more attention is being paid to building the pipeline this year. Along those lines, the third activity respondents identified as helping to drive positive results next year is tied to making improvements to and investing in both their sales and marketing functions.

Perhaps reflecting the need to balance aggressive activities like new customer acquisition and marketing overhauls with cost containment, the no. 2 area that channel firms believe will be needed to contribute to a more optimistic outcome next year is to improve internal operations. In other words, get more efficient. Whether that is streamlining internal processes—something critical to a well-run managed services firm, for example—or deploying new automation technologies, the quest for operational efficiency is an ongoing component of optimal business performance.

Rounding out the list of items companies deem essential to a positive 2023 include the successful launching of new business lines and a return to normal economic conditions that see inflation decrease and supply chain woes abate. One could argue that these two factors are interdependent, given that a rough macroeconomy might be considered a poor environment for new business ventures. But that isn’t always the case. An attribute of many firms that weather a general economic storm well is their propensity to double down on investments in new things. And a new business line does not necessarily mean new products to sell (though it can). It could reflect a shift to a different business model, which will be discussed later in this report.

As discussed in the 2023 trends outlined in this report, inflation looms large for the channel. Among the factors that could lead to a pessimistic year ahead, continued high inflation, cited by 41% of respondents, led the pack. The remainder of the list includes 34% that cite concerns over growing labor costs and the need to find workers with the right set of skills for today’s tech world, 32% that worry about any unexpected geopolitical or macroeconomic shock to the system, and 30% that fret about customers postponing technology purchases. The cause-and-effect element of these concerns is undeniable. Increased inflation or other economic shock could beget recession, which could, in turn, result in layoffs that upend the labor market and curtail customer spending. Or the reverse could happen. So far, it’s been unpredictable.

One point of interest from the list of factors that arouses pessimism is the relatively low ranking of automation as a hurdle. Just 18% cite automation as a potential threat to growth in the year ahead. As elaborated in one of this report’s trends, it’s clear that automation is a development that is more positive than negative. With some caveats, of course.

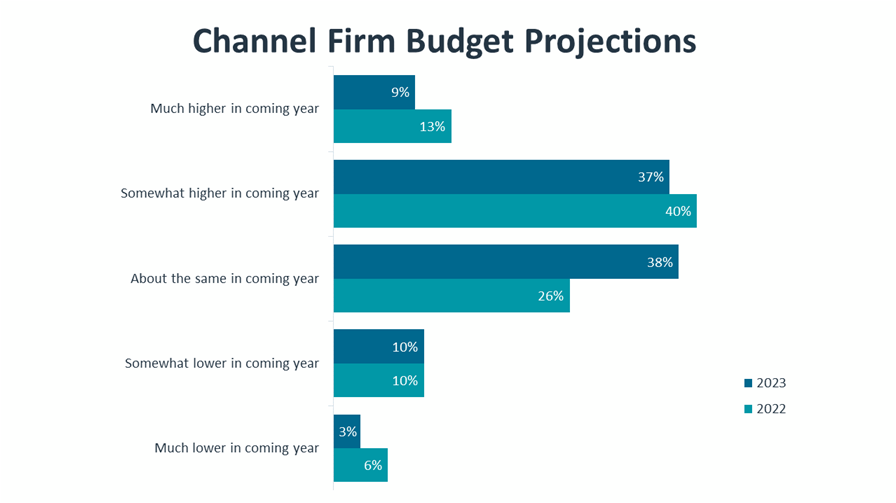

Let’s talk about budgets. Much like general sentiment about prospects for the year ahead, many channel firms are making positive, yet cautious, predictions about their upcoming budgets. Compared to last year, when 53% of respondents said budgets would be higher (either much or somewhat) in the year ahead (2022), a slightly lower 46% said so this year. And whether indicative of caution, pragmatism, or both, 38% of this year’s respondents expect budgets to come in flat or about the same as the year before. This compares with the 26% that predicted this last year. Clearly, the economy’s uncertainty factor weighs on prognostication here, but fewer firms than last year are expecting decreases to their budget (13% vs 16%, respectively).

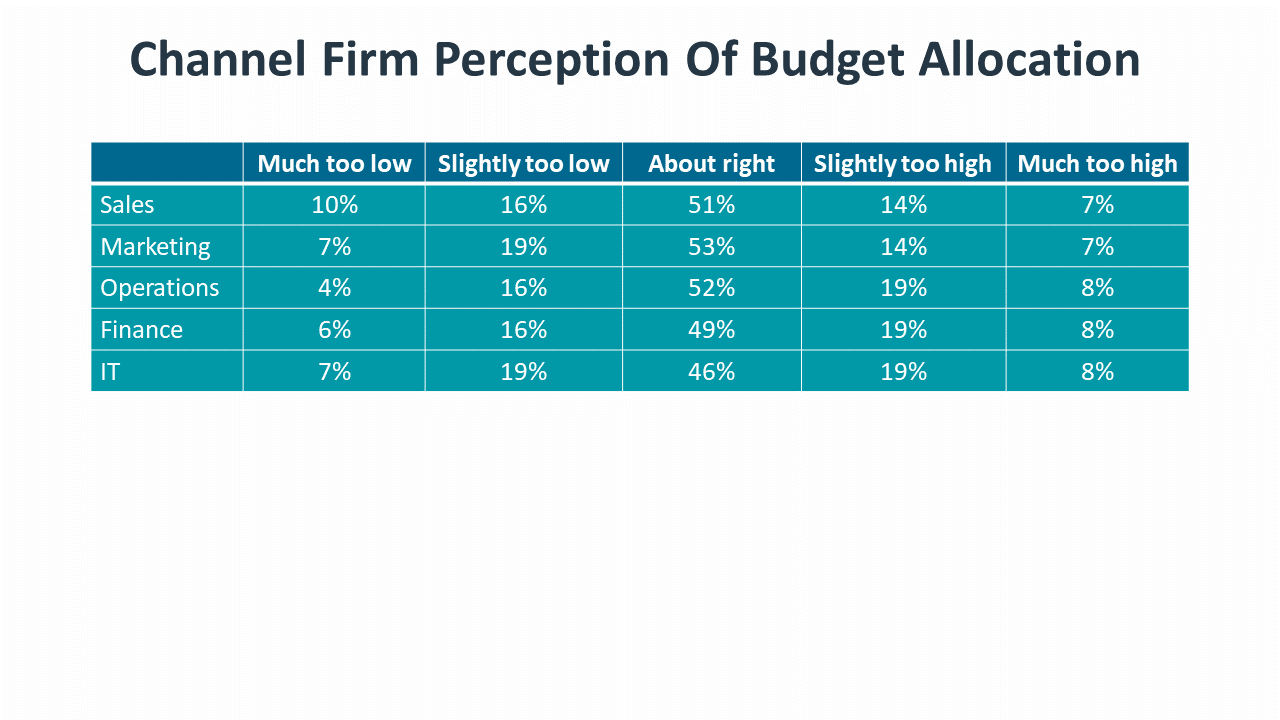

Most respondents are relatively content with the amount they are currently spending in various functional areas of their business. Roughly half of the respondents said spending is “about right” for sales, marketing, operations, finance, and IT at their companies.

If pressed to identify areas where spending is too low, a slight edge goes to sales, marketing, and IT functions. Sales and marketing, as indicated above in this report, are considered areas to spend in 2023 to ensure growth and profitability. For many channel firms, marketing has lagged in both resource allocations and general attention. Few channel firms employ a full-time marketing staffer, and the discipline itself has often been overlooked. However, on the bright side, data from the last several years shows a more concerted effort around marketing and branding. Baby steps.

Interestingly, between 21% and 27% of respondents believe spending is either slightly too high or much too high across all five functional buckets. Given that respondents to the survey come from all disciplines within an organization – from the business side of sales, finance, and marketing to technical employees to managers and business owners – this parity of agreement is somewhat novel. Again, the unifying driver may be economic uncertainty as we enter 2023. Every job role within an organization might be looking for ways to save money, reduce costs, etc.

All that said, channel firms have their spending priorities for the year ahead. Some of them reflect strategic external initiatives, others the fuel for operational improvements on the inside. Call this the yin and yang that comprise a high-performing company.

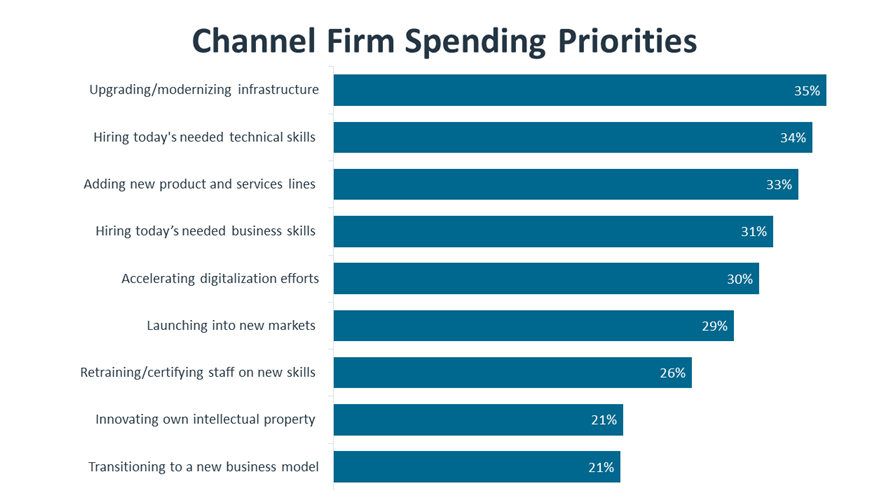

Topping the list is updating and modernizing current infrastructure, which 35% of respondents identified as a spending priority. This is an interesting one given that infrastructure improvements have been a focus area throughout the span of the pandemic, when many companies throttled back on new endeavors and instead spent time and money shoring up their own operations, as well as refreshing the basics for their customers. Clearly, that mission is not complete.

On par with infrastructure improvements in terms of spending priorities is hiring staff with the right technical skills for today’s digital world, which 34% of respondents cited, as well as adding new product and service lines of business, which 34% identified. The workforce issue is perennial but critically important. As companies jockey against the competition, they will need to up their game by hiring employees skilled in job roles in demand, such as those in data, cybersecurity, and emerging trends. Software acumen, specifically development skills, will also play a larger role in the channel’s typical talent needs in 2023. Spending priorities aren’t just centered on the technical workforce, though. Thirty-one percent of channel firms said they will spend to seek skilled sales and marketing employees in the next year. This would include sales reps who are adept at selling services and consulting contracts, along with marketing professionals with expertise in social media and other omnichannel approaches to customer communications.

Speaking of customers, understanding their needs, spending priorities, and constraints is a crucial ingredient for channel success in the new year. For years now, the industry has seen a slow but steady shift in who holds the purse strings when it comes to technology decision-making and procurement. More and more business executives today own tech budgets and routinely make critical purchasing decisions for their departments and staff – both with and without the involvement of an internal IT department. This has necessitated change within channel firms seeking to work with these customers, especially with respect to sales techniques and activities, as well as marketing messaging and the choice of conduits for communication.

Channel firms rely on some approximation of what customer budgets for technology look like each year. It’s been a crapshoot of forecasting for many firms during the pandemic, especially those that count the small end of the SMB market as their primary customers. Those SMBs were hard hit during the pandemic, and their tech spending, in many cases, dropped off. Still, patterns were unpredictable. For some customers, the unforeseen remote work migration forced a wave of spending on devices, Wi-Fi, and other virtual communications apps. Still,l others turned to the services of an MSP for the first time ever.

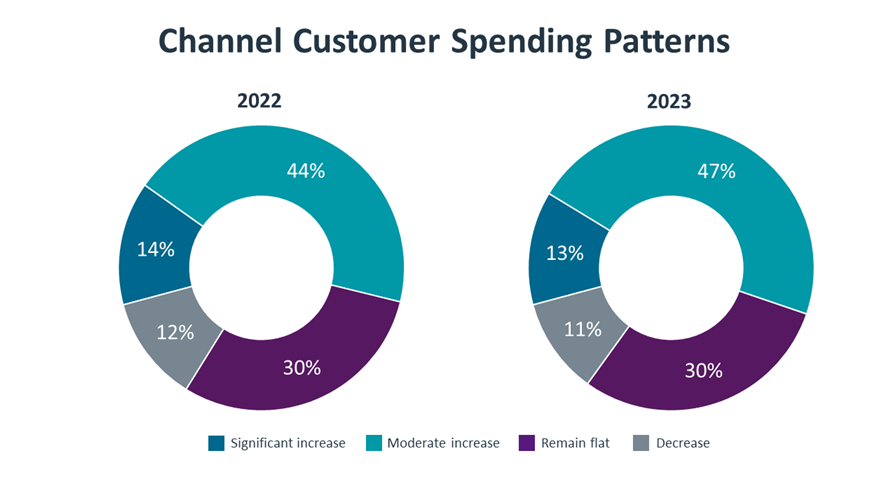

Diving into the data, channel respondent predictions for customer spending on technology in 2023 mirrors nearly exactly what they saw for real in 2022. That’s a safe assessment on their part, again likely reflecting the economic unknowns ahead. Depending on how things go with inflation and other economic variables, customer spending on technology could surge past or retreat from these predictions.

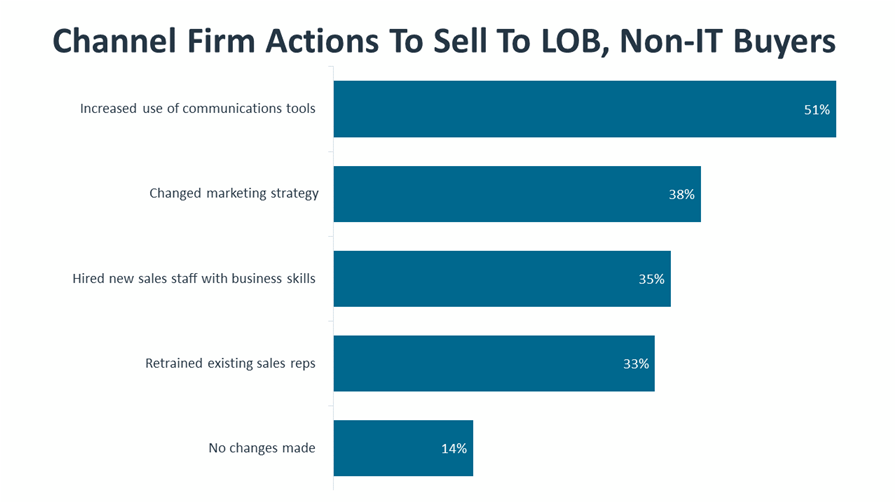

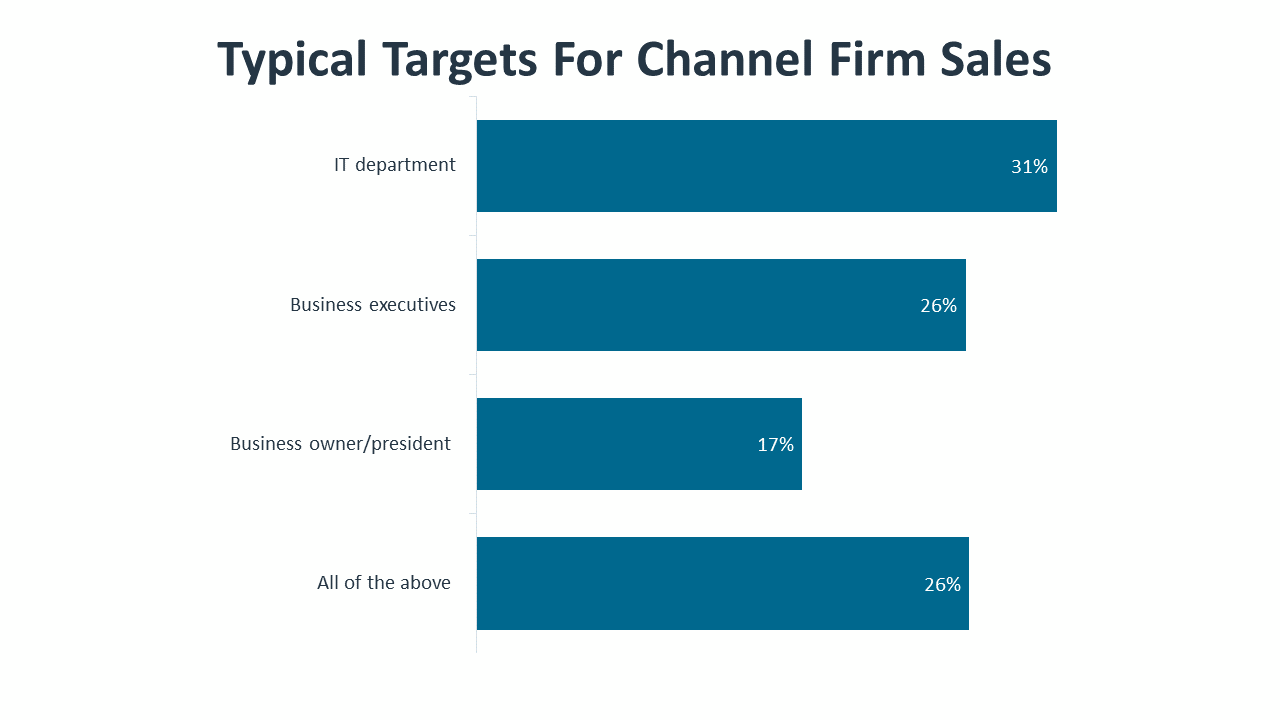

What is completely clear is that everyone today is a potential customer of technology. Consider the following: 17% of channel firms said they sell to a business owner/president, 26% sell to business executives, 31% sell to an IT department person, and 26% sell to all three. This means the days of speeds and feeds tech talk as the main sales call vernacular to the IT guy are largely over. Buyers today want a channel provider that has unique knowledge of their business mission, operational needs, and goals. The shift in conversation toward business outcomes is a learning curve for many channel firms, but the skill will be essential moving forward as part of overall improvements to customer experience and sales effectiveness.

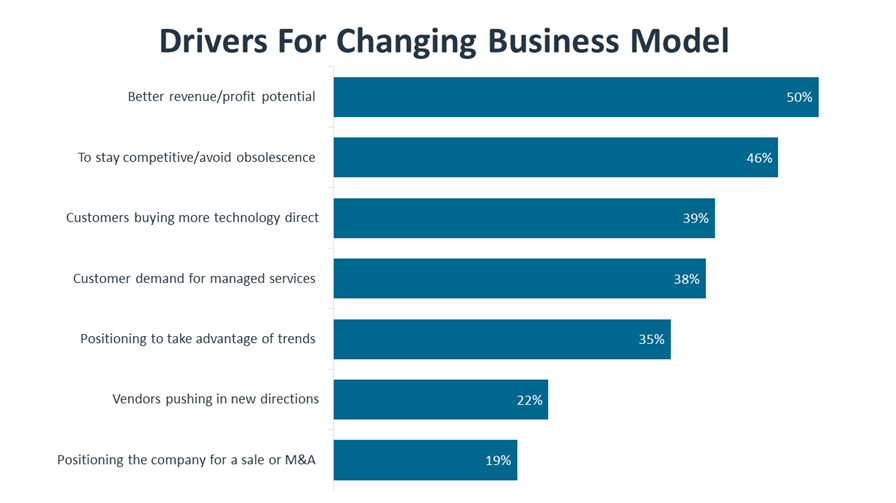

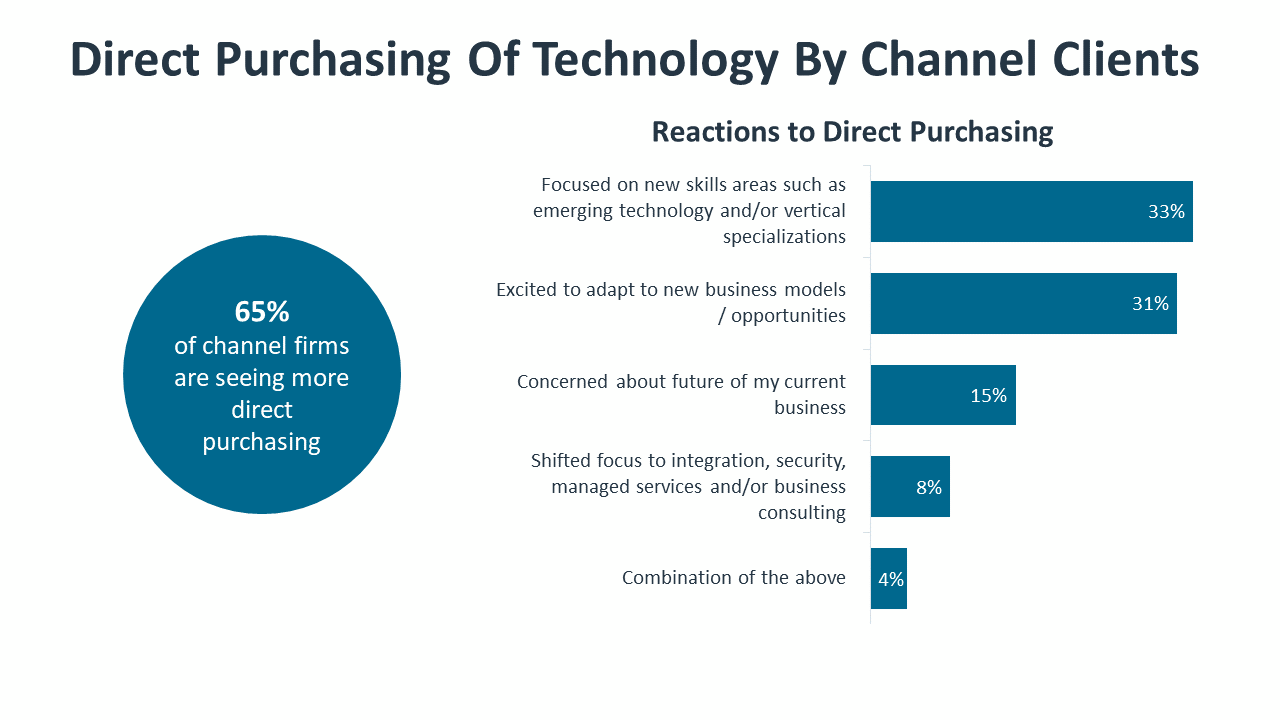

Business models are changing for the channel just as the customer is. For years, we have been hearing about and witnessing a slow march from traditional reseller of hardware to full-portfolio solution provider to managed services provider. That is very much still happening. But the drumbeat for business model change seems louder today, largely driven by a digital-everything economy, cloud computing, hardware commoditization and margin erosion, and direct procurement competition from online marketplaces and vendors.

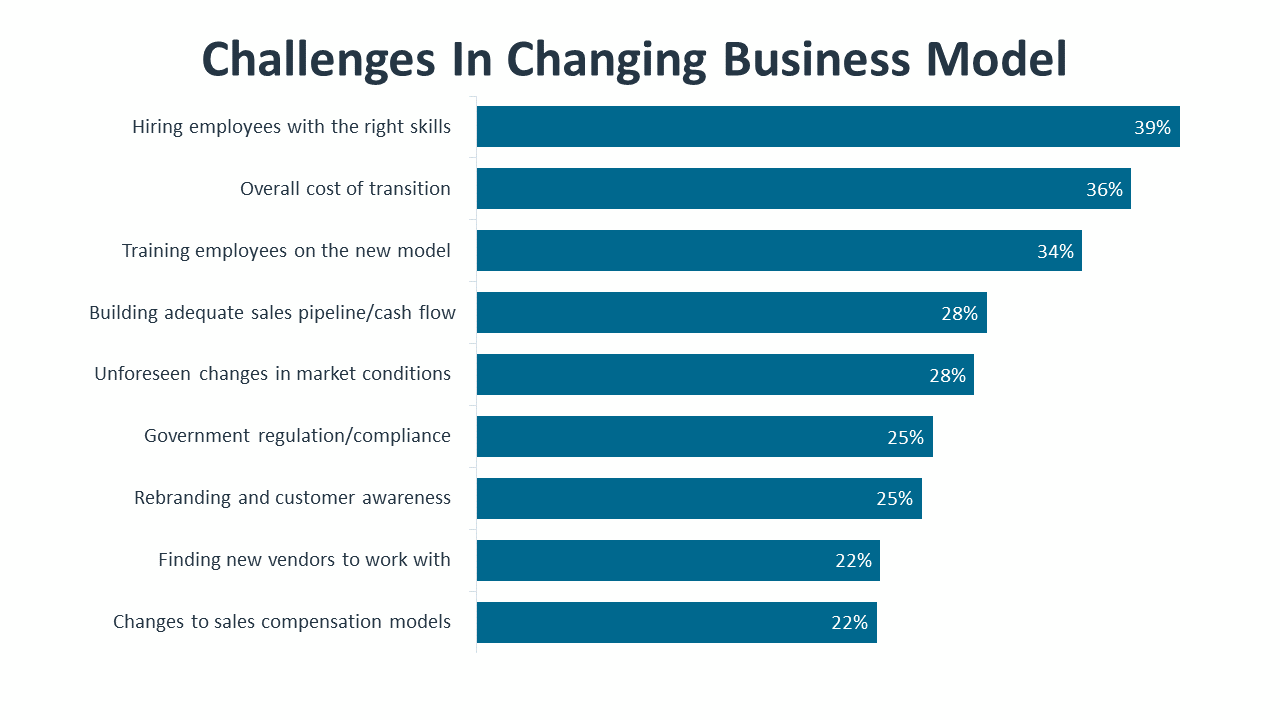

Business model change can mean many different things to many different channel firms. A small tweak such as adding a vertical specialty, for example. Or a major transition from a product reseller to a company that does pure IT consulting. Whatever it happens to be, most channel firms today report some degree of business model change or active consideration of starting one.

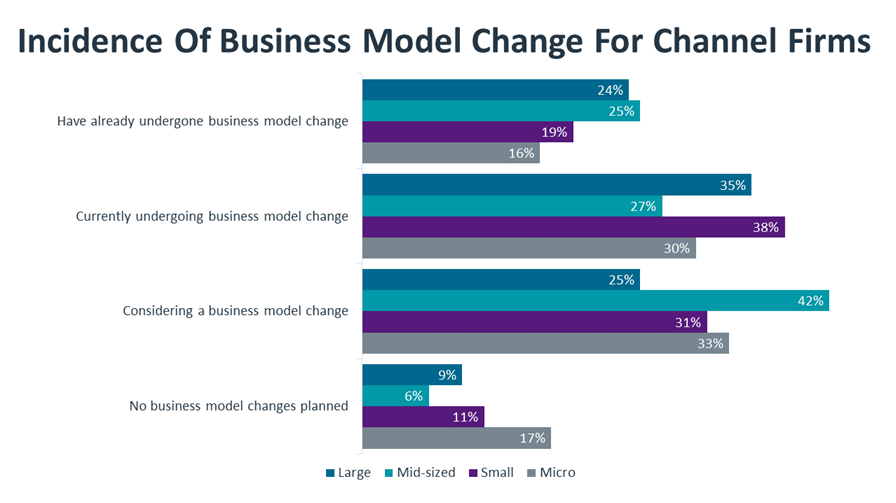

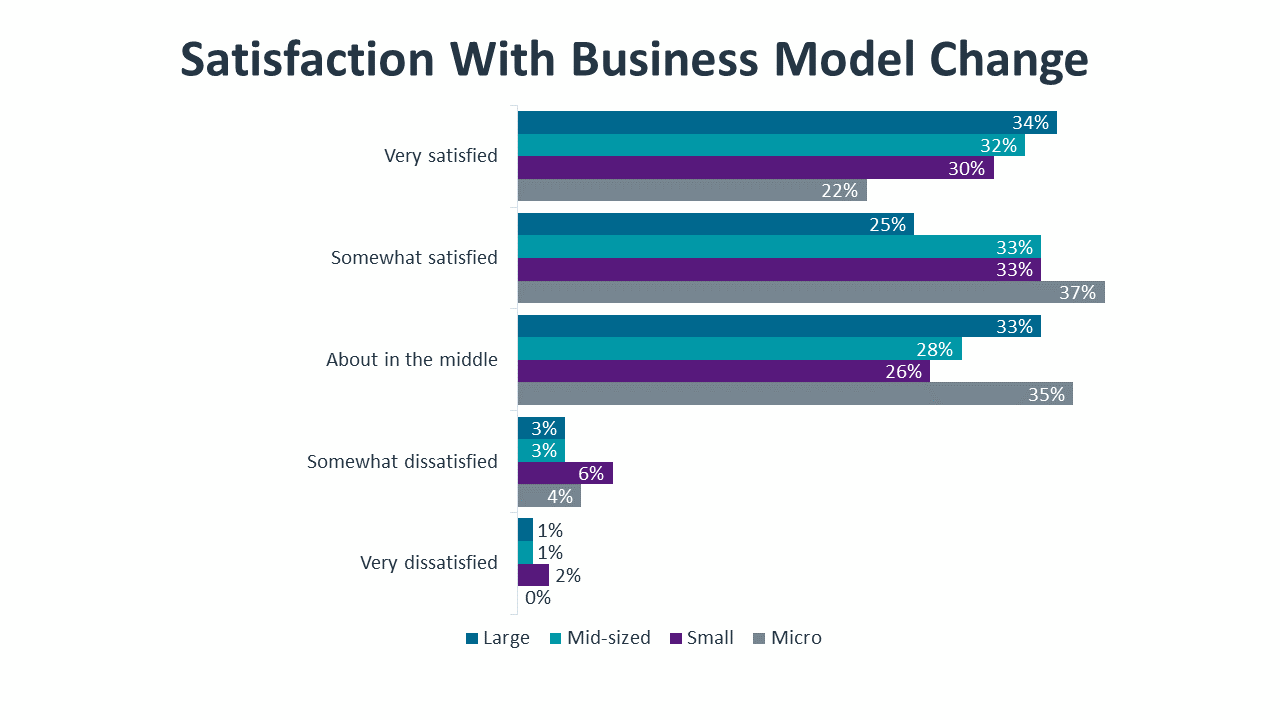

Twenty percent of respondents said they have already undergone a change to their business model in the last few years; 35% are in the middle of one, and 32% are currently exploring one but have not yet started. Just 11% said that no business model talks are on the table at this time. Larger firms are ahead of their smaller brethren in terms of completed business model shifts, which is not surprising given their access to greater financial resources and the ability to pilot project new initiatives while keeping their original business going. Small firms typically just can’t do that. That said, a net 68% of micro- and small-sized channel respondents said they were currently undergoing a business model transition.

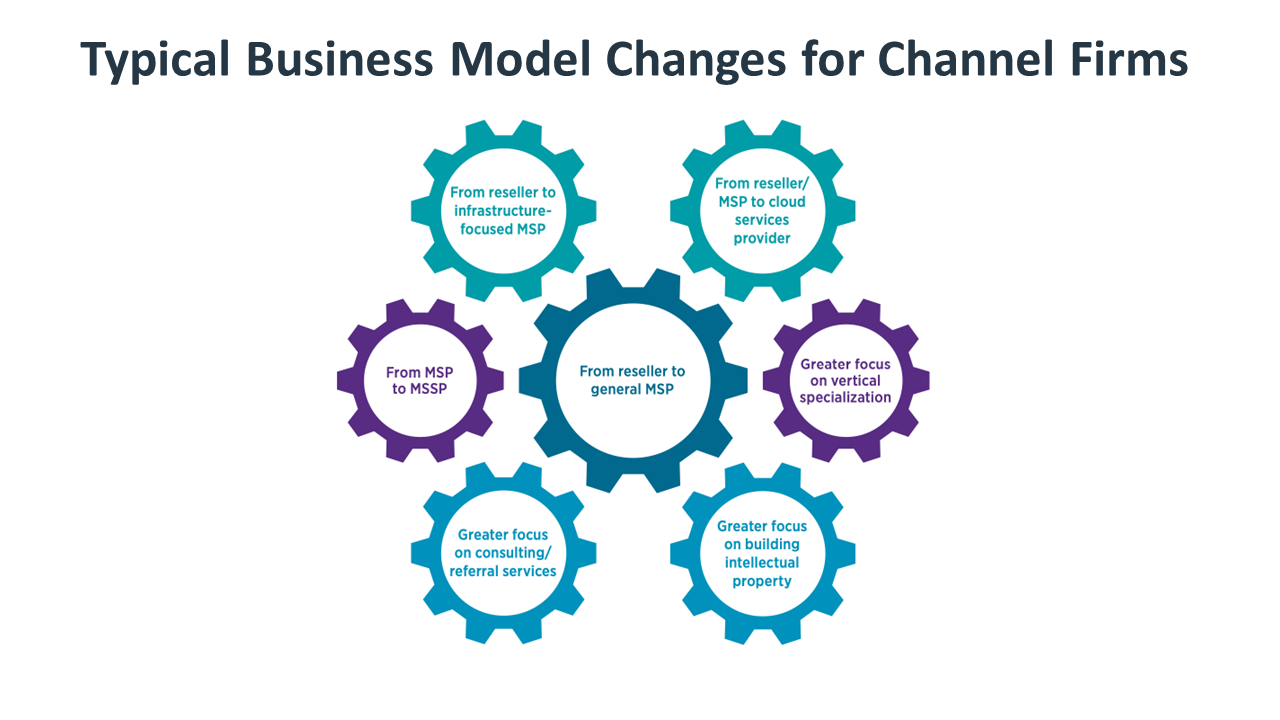

What do these business model changes look like? For the most part, they are variations on a theme: The move to recurring revenue and services. But the flavors are nuanced. Here are the top five business model shifts respondents reported:

- Product reseller to MSP selling everything from infrastructure to business applications to emtech services

- Transition to a combination of different business models

- Product reseller to traditional MSP selling infrastructure services (devices/network)

- Product reseller to cloud services provider managing SaaS and other cloud-based workloads for clients

- Transition to an IT referral or consulting business

This journey to recurring revenue and, most importantly, services has been ongoing. But today’s realities have elevated the urgency of moving faster. More customers buying directly from online marketplaces have many in the channel scurrying to find their competitive play when they no longer own the initial transaction. That play takes the form of pre- and post-sales services, including work around integration, cybersecurity, compliance, and ongoing management of the customer environment.

And let’s not forget the financial piece of the picture. Services are lucrative and certainly more profitable than hardware sales today. They also bond channel firms to their customers, whether through ongoing project work or managed services. This customer stickiness and familiarity has been one of the channel’s greatest assets over the years. It’s also one that holds up during the ebbs and flows of an uncertain economy.

Appendix

Please note this is an excerpt, and the full report contains more detail.

Methodology

This quantitative study consisted of two online surveys fielded to business and IT professionals during September/October 2022. A total of 500 professionals based in the United States participated in each survey, yielding an overall margin of sampling error at 95% confidence of +/- 4.5 percentage points. For international regions (ANZ, ASEAN, Benelux, DACH and UK), a total of 125 professionals in each region participated in each survey, yielding an overall margin of sampling error at 95% confidence of +/- 8.9%. Sampling error is larger for subgroups of the data.

As with any survey, sampling error is only one source of possible error. While non-sampling error cannot be accurately calculated, precautionary steps were taken in all phases of the survey design, collection and processing of the data to minimize its influence.

CompTIA is responsible for all content and analysis. Any questions regarding the study should be directed to CompTIA Research and Market Intelligence staff at research@comptia.org.

CompTIA is a member of the market research industry’s Insights Association and adheres to its internationally respected Code of Standards and Ethics.

Read more about tech industry sectors.